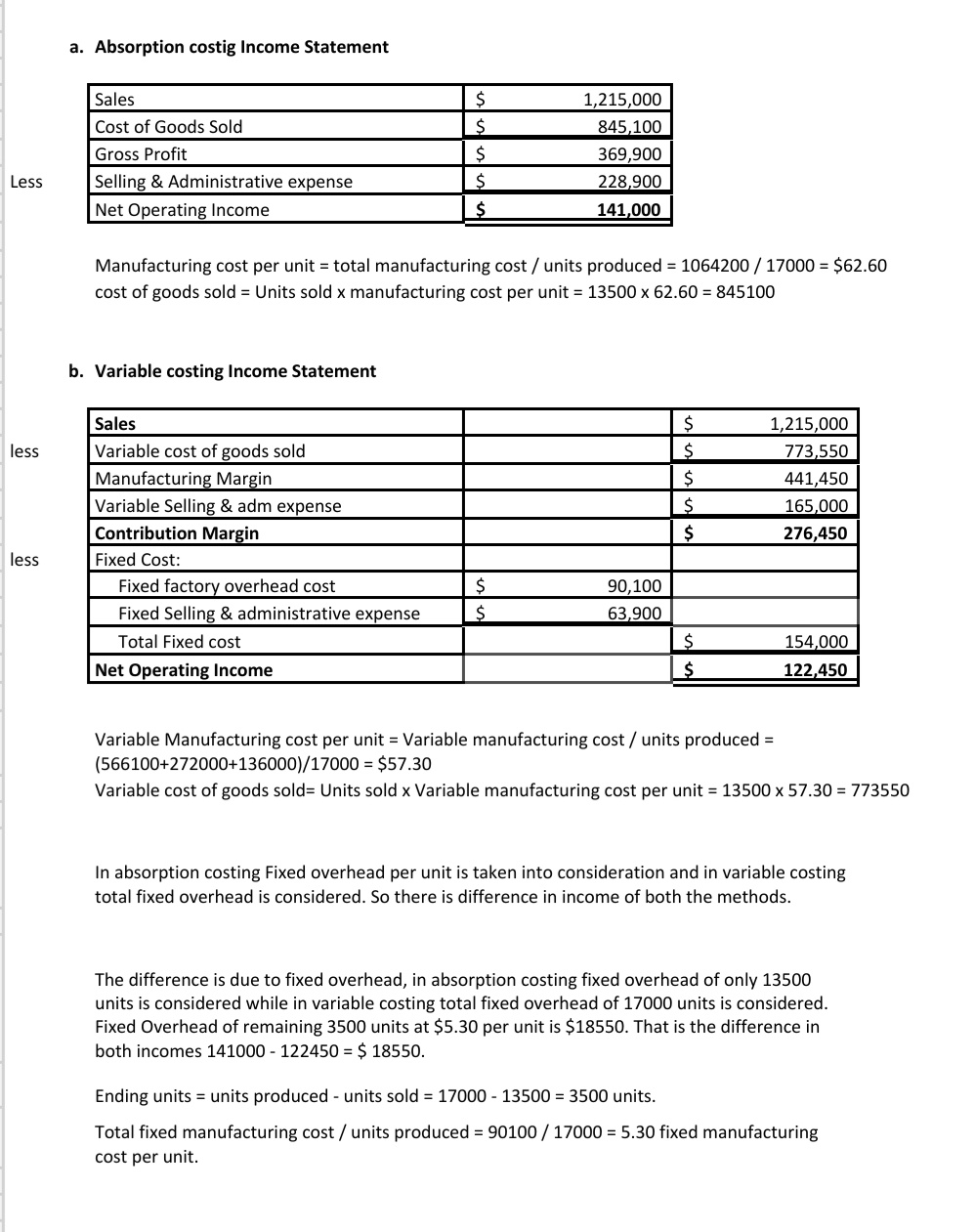

It helps companies determine the full cost of producing a product or service. The cost of goods sold (COGS) is calculated when the ending inventory dollar value is subtracted. To compute net operating income for the period, subtract selling expenses.

Conclusion: Embracing Accurate Accounting with Absorption Costing

Every other part of the income statement becomes easy to calculate once you have gotten your cost per unit. It is important to note that the variable items are only calculated based on the number sold. This means that cost can only be expensed based on the amount sold while unsold items end up in the inventory. Most people, especially those in accounting, would have questions to ask about absorption costing and income statements. Absorption costing is often used interchangeably with the term full costing, and they are usually identified to have similar meanings. In the article about income statements under marginal cost, we discussed that marginal costs give a higher net profit figure as compared to absorption costing.

Introduction to Absorption Costing in Accounting

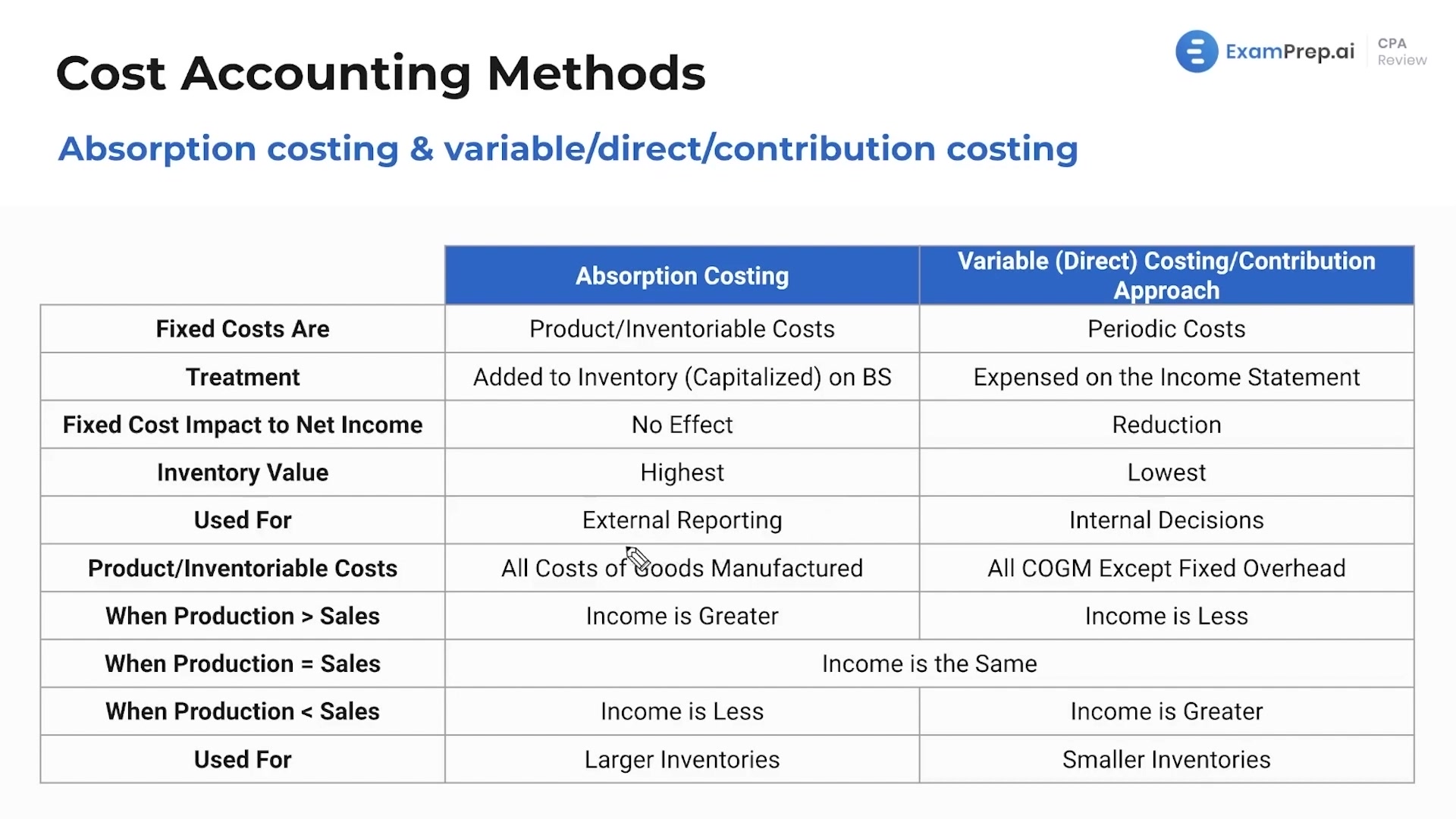

The absorption and variable costing methods are the two major methods that firms use to increase work value in the process and finished goods inventory for financial accounting. The variable cost could also be referred to as direct costing or marginal costing, and it includes all variable costs like direct labor, direct materials, and variable overhead. Here, these variable costs are assigned to products and fixed overhead costs for some time. Under absorption costing, each unit inending inventory carries $0.60 of fixed overhead cost as part ofproduct cost. Therefore, ending inventory under absorption costingincludes $600 of fixed manufacturing overhead costs ($0.60 X 1,000units) and is valued at $600 more than under variable costing. The difference between the absorption and variable costing methods centers on the treatment of fixed manufacturing overhead costs.

Variable Costing Versus Absorption Costing Methods

- This causes net income to fluctuate between periods under absorption costing.

- Variable selling andadministrative expenses are not part of product cost under eithermethod.

- The U.S. Securities and Exchange Commission (SEC) and GAAP are primarily concerned with external reporting.

- As we all know, absorption costing is also known as full cost accounting because, under this method, all of them directly attributable costs of production are included.

- These costs include raw materials, labor, and any other direct expenses that are incurred in the production process.

Absorption costing is by GAAP because the product cost includes fixed overhead. It is not by GAAP because the fixed overhead is treated as a period cost and is not included in the cost of the product. Companies, however, can get information from variable costing and absorption costing systems as long as the companies can calculate the amount of every manufacturing fixed overhead per unit. Absorption costing means that every product has a fixed overhead cost within a particular period, whether sold or not.

5: Compare and Contrast Variable and Absorption Costing

If you remember marginal costing, you will remember that we used the sum of marginal variable costs. Therefore, you should treat the selling and administrative costs like a mixed cost. In this case, the variable rate is $5 per unit and the fixed cost is $112,000. Write your cost formula and plug in the number of units sold for the activity. According to accounting tools, the primary item on an absorption income statement is gross revenues for the period. To calculate COGS, add the cost of products produced for the time to the dollar worth of initial inventory.

Advantages and Disadvantages of the Variable Costing Method

The key difference from variable costing is that fixed production costs are included in the inventory valuation and expense recognition under absorption costing. Careful COGS calculation as per GAAP standards is essential for accurate financial reporting. Absorption costing and variable costing are two different methods of costing that are used to calculate the cost of a product or service.

The accountant’s entire business organization needs to understand that the costing system is created to provide efficiency in assisting in making business decisions. Determining the appropriate costing system and the type of information to be provided to what is a credit memo definition and how to create management goes beyond providing just accounting information. The costing system should provide the organization’s management with factual and true financial information regarding the organization’s operations and the performance of the organization.

Absorption costing is an accounting method that captures all of the costs involved in manufacturing a product when valuing inventory. The method includes direct costs and indirect costs and is helpful in determining the cost to produce one unit of goods. Compared to variable costing, absorption costing income statements tend to show less volatility in operating income from period to period. This is because fixed costs are smoothed into COGS rather than impacting the period they are incurred. Absorption costing considers all fixed overhead as part of a product’s cost and assigns it to the product.

The traditional income statement, also known as the absorption costing income statement, is created using absorption costing. Costs are divided into product and period costs in this income statement. It is a conventional technique for estimating the costs of the services and goods produced. Unlike variable costing, it covers fixed costs and inventories while calculating the cost per unit. Each unit of a produced good can now carry an assigned total production cost. This eliminates the distinctions between fixed and variable costs, thereby reflecting the impact of overhead on manufacturing.

This leads to an accurate representation of product cost on the income statement. Therefore, to calculate the product costs under absorption cost, the direct materials, direct labor, variable and fixed overhead would be added together to produce the total cost. These costs can also be calculated according to each unit, and this is done by dividing the total product cost from the total unit produced.