Down-payment

Such as for example, if you are purchasing a house to own $100,000 the lending company will get charge you a downpayment off 5%, so that you was expected to enjoys $5,000 inside the bucks due to the fact downpayment purchasing the house. Their home loan carry out after that become to have $95,000, the price of the home with no off fee.

Dominating

Very lenders has old-fashioned home loan guidelines that allow you to use a certain percentage of the worth of your house. The brand new part of principal you might borrow usually differ considering the loan program you be eligible for. Oftentimes, a traditional home loan tool requires 20% down and allow one use 80% of your worthy of.

You will find special apps for earliest-time homebuyers, experts, and reduced-income consumers that permit reduce repayments and better percentages out of principal. A mortgage banker is also remark these types of options along with you to see for many who meet the requirements during the time of application.

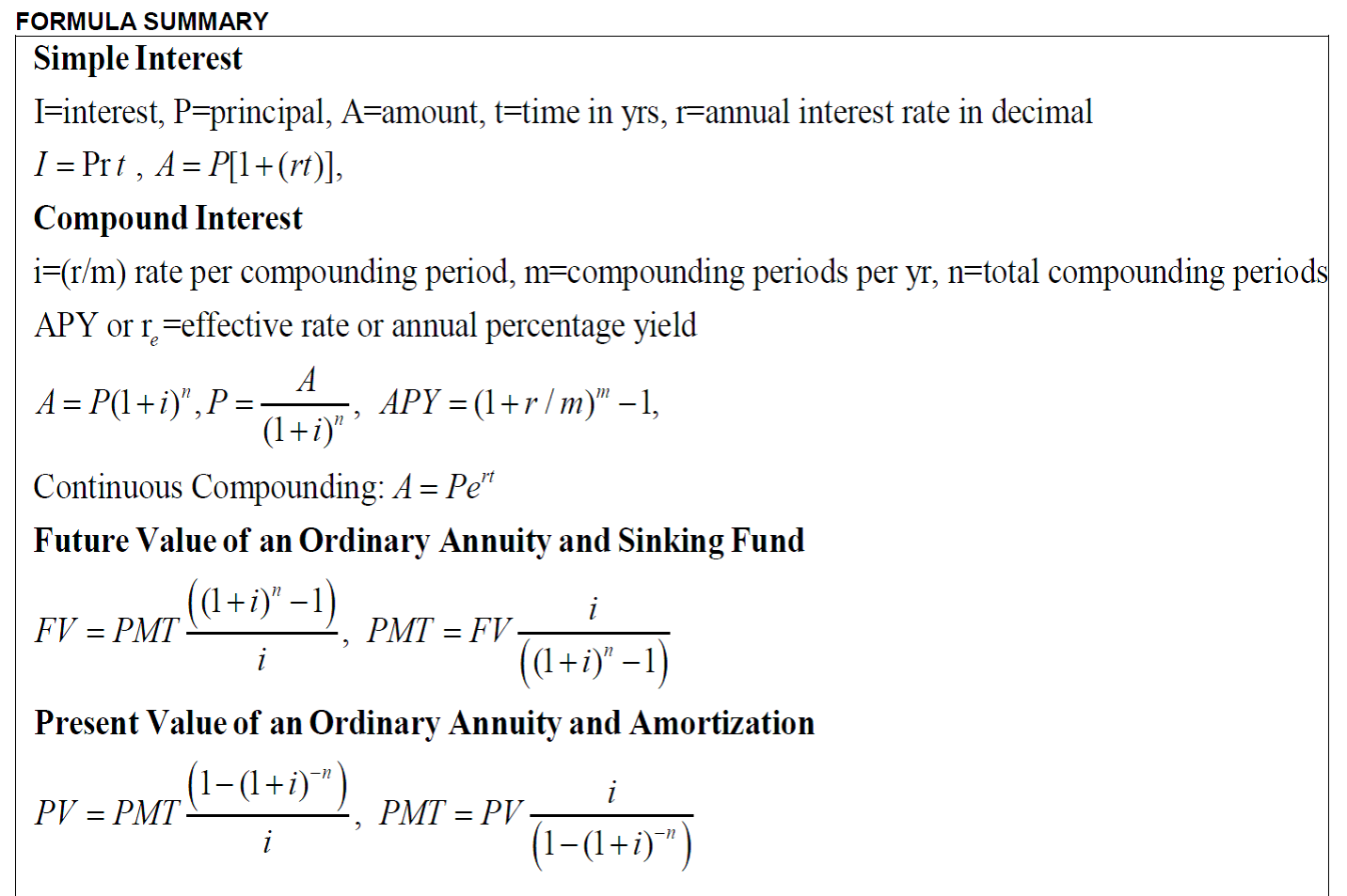

Attention

If you were to take out a 30-season (360 days) mortgage loan and you can use that same $95,000 from the more than example, the quantity of desire might spend, for those who made all the 360 monthly premiums, could be a small more $thirty two,000. The monthly payment because of it loan would-be $632.

Taxes

When you own a house or assets you will have to pay possessions taxation to the county where in fact the home is discovered. Very loan providers will need you to shell out your fees with your mortgage repayment.

The financial institution usually divide the $step one,000 by the 1 year and you will add it to their commission. This should mean $ thirty days. Your own monthly payment with taxes included create next getting $ + $, having a whole payment out-of $.

Escrow

The financial institution will pay your property fees for your requirements every six months when they are due, making use of the funds from the escrow membership. As they are expenses they and also in handle, this might be good-for the financial institution, because they’re hoping that the collateral isnt vulnerable to non-percentage away from taxation.

This is exactly including very theraputic for this new resident since it allows all of them so you can funds the taxation month-to-month however have to pay it all-in-one lump sum out-of $step one,000, or twice yearly as numerous counties require ($500).

Insurance coverage

Loan providers requires the fresh new resident for suitable insurance policies toward their home. Again, because home is named collateral of the bank, they wish to make sure that it’s safe. Property owners are required to incorporate a duplicate of one’s insurance rates rules on financial.

Inside our analogy, $1,two hundred a-year split because of the 1 year would be $100 thirty days. Your own commission today carry out boost of the $100 to another complete regarding $-$600 in principle, $thirty-two when you look at the attention, $ within the taxation, and you may $100 for the insurance rates.

The financial institution retains it profit a comparable escrow account as the your home fees and produces money with the insurance company on your account.

Settlement costs

- Assessment can cost you to determine the worth of your residence.

- Name or courtroom will cost you incurred having researching or getting ready the brand new records for your mortgage.

- Credit reporting charges for pull and you may looking at your credit history.

These types of costs compensate brand new lenders or originators who help the brand new software and you can closure process, new group which opinion and underwrite the application, and you will activities involved in regulatory compliance.

Origination Fees

Origination charges, known as app fees, might be a fixed amount otherwise a portion of one’s mortgage amount (usually 0.5% to one%).

Underwriting Charge

If for example the bank imposes fees to possess underwriting or running, they are often fixed amounts that differ with respect to the mortgage dimensions and you will/otherwise financing program used.